And avoid becoming a victim

COI’s provide a gateway to identity theft and scams for would-be thieves.

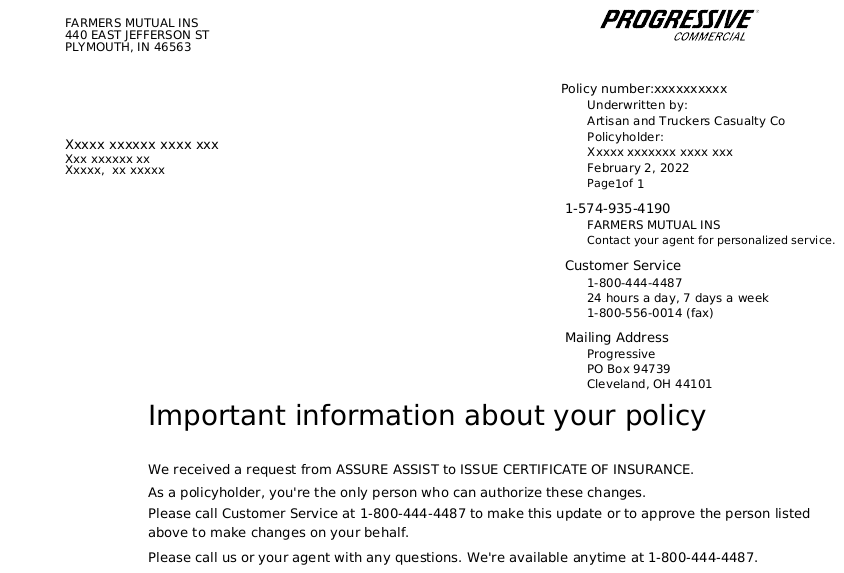

Way too often I get calls from someone claiming to be a broker who wants to receive a certificate of insurance for one of my customers so they can dispatch them on a load. I politely inform the broker, “COIs can only be requested by the insured.”

Then: I contact the customer to inform them of the broker attempting to get a COI. Frequently, that’s when I learn that the supposed dispatch didn’t and wasn’t about to happen at all — it was either an attempt at identity mining or a scam.

Many of us look at our COI and think, “there’s nothing here to steal my identity.” That is most certainly not the case. Would-be identity thieves use multiple sources to mine or gain as much information on us as possible before executing the theft. Our COIs contain our addresses, company names, insurance policy numbers, vehicle identification numbers, our insurance carrier, our insurance agency information and more.

Insurance fraudsters and insurance stalkers can also use COIs to determine if it’s worth their time to attempt an insurance claim or lawsuit against us. We all know what an insurance fraudster is. But I call attorneys who target trucking companies insurance stalkers. Both like to use COIs to identify who they can collect the largest sum of money from with an insurance claim or lawsuit. Insurance stalkers can use COIs when a potential client approaches them with a request to represent them for a claim or lawsuit involving a truck or trucking company.

The FMCSA only requires the minimum bodily injury property damage (BIPD) coverage to be listed on our publicly available MCS-90 endorsement. However, that amount may be and frequently is less that what our actual policy BIPD coverage is for. These days, most trucking companies have at least $1 million in BIPD coverage. That is why insurance stalkers like to have a COI, because it shows that full amount of BIPD coverage on the policy. Insurance stalkers use that information to adjust the amount of the claim and/or lawsuit to an amount closer to the total BIPD coverage of the policy.

Insurance fraudsters, meantime, can use COIs to identify which trucks they wish to target in a planned “accident” — aka insurance fraud.

Broker and carrier impersonation are forms of scams previously reported on here in Overdrive. I can think of several ways to use a COI to accomplish many identity-theft crimes and scams. Because I do not want to not give a would-be scam artist or an aspiring identity thief a new idea, I’ll limit my list to the most obvious and simple ways our COIs can be used against us.

After acquiring your COI…

- The identify thief learns your preferred lanes of travel from the load boards, contacts you and says he has a great load, already has your COI and only needs a current W9 to dispatch you on the load. When the would be identify thief receives your W9 they now have the most important piece of information to steal you or your company’s identity.

- The would-be thief learns your preferred lanes of travel from the load boards, contacts a broker on a load, posing as you, accepts the load and receives an advance — a scam that’s grown more common in recent years and is often referred as the fuel-advance scam. Fundamentally, though, it’s about identity theft, and you may be held liable for the advance and required to refund the broker for their loss in the worst cases.

- The would-be thief uses the learned information for a loan in your name and uses the VIN number on the COI for collateral, securing the loan in your name. When the loan goes unpaid, your truck may be at risk of repossession by the lender.

These are but a few scenarios. I’m certain that enterprising scam artists and identity thieves have more ways to use information on the COI against us than I can think of. The good news is there are steps you can take to protect yourself.

- Verify with your insurance agent they will not give out any COI for your policy unless the request comes directly from you.

- Remove all “additional insureds” from you policy. Along with other risks of having additional insureds, such insureds can potentially request COIs be given to third parties without your knowledge.

- Lock all your credit reports to prevent creditors from receiving a credit report for a would-be identity thief posing as you.

The last may well be the most important among these – and you can do that via the links below to credit-freeze services of the major credit-reporting services:

Equifax | TransUnion | Experian

Taking that final step may seem drastic but it won’t cost you in hard cash and it’s something I have done myself. It will however create more work for you when applying for credit of any kind. You’ll have to unlock your credit temporarily to allow for a legitimate lender or other entity to access the report, before locking access again. But in today’s world, with identity theft running rampant, that little bit of headache could be well worth the effort.

To get more great business tips and trucking news visit Overdrive extra!