LearnToTruck.com

How to Lower Insurance Premiums

Yes, you can reduce your insurance premium … and I have the customers to prove it!

By exercising good safety practices and being proactive with all insurance policies, four of my insurance customers have all recently been rewarded with lower insurance premiums. Not a one of them had to increase their deductibles, lower the stated value of their trucks, remove coverage or anything else. At renewal, their premiums simply went down! Read more...

The Need for COI Security

Cargo theft is no longer a crime of opportunity - it’s a coordinated,

evolving operation that’s quietly siphoning millions from freight brokers,

shippers, and carriers. According to Chad Eichelberger (pictured),

president of Reliance Partners, the industry is facing an unprecedented

wave of fraud, marked not just by its scale but by its sophistication.

“The fraud that’s going on in the space right now is at epidemic levels,”

Eichelberger said. “Compared to what we witnessed in the past, it’s

evolved dramatically.” Read more...

Don’t be lured into dishonesty to reduce your insurance premiums

Recently a gentleman from Indiana contacted me. He said he was starting his own trucking company and would like a quote for insurance. He said he had prior experience owning a trucking company and was looking to re-enter the industry.

I submitted his application to several insurance companies as I typically do, to see which insurance carrier would provide him the lowest premium for the amount of coverage he was seeking. To my surprise ALL insurance carriers “declined” (a polite word for refused) to offer an insurance quote. Read more...

Deception Wreaks Havoc… Again!

From time to time I am contacted by a customer about a cargo claim. This year has been no different. Some of those calls include concerns about a letter of declination for a recent cargo claim. Sad to say, my answers to those customers are usually not what they want to hear.

An insurance policy is actually a contract between the insured and the insurer. Contracts (the insurance policy in this case) always come with a set of terms and conditions. When one party of the contract violates a term or condition of the contract then the other party is no longer obligated to fulfill their part of the contract EXCEPT where required by law. Read more...

New Jersey State Government Created Chaos

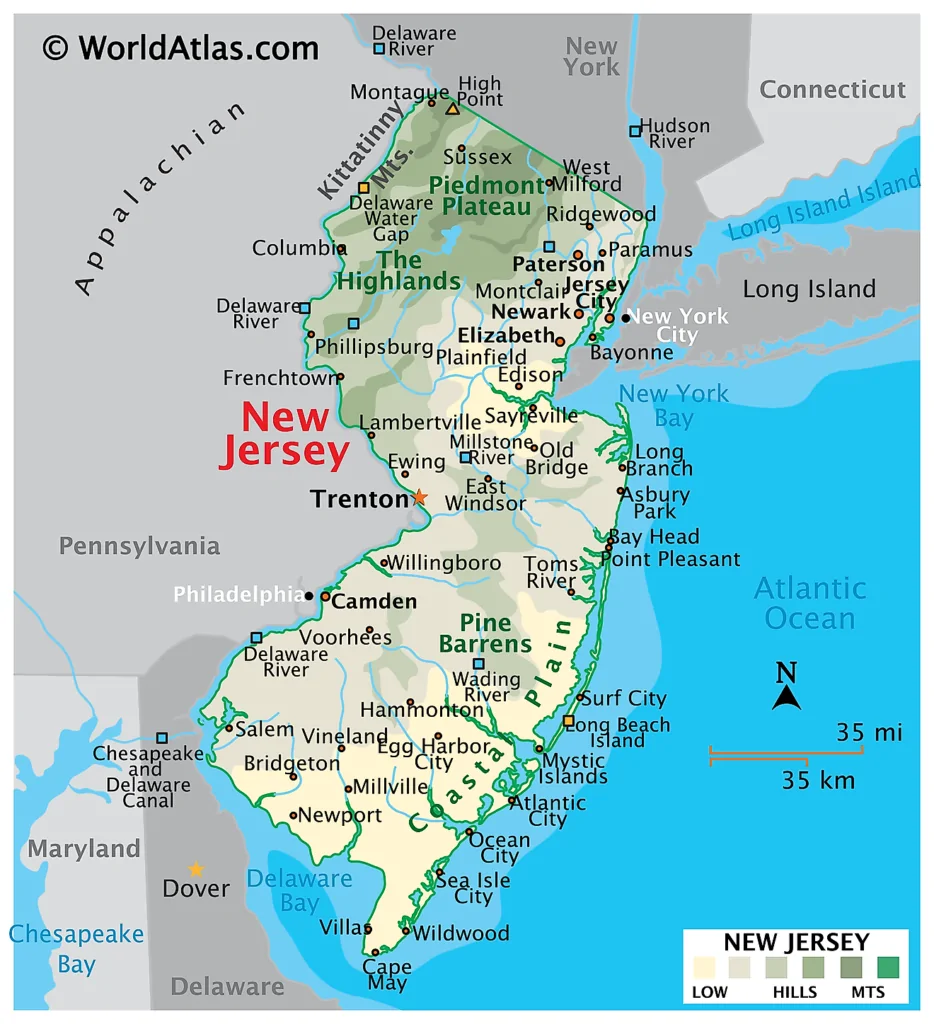

New Jersey has new increased minimum BIPD insurance coverage for all commercial vehicles that travel into or through New Jersey.

Each insurance company is addressing New Jersey’s new insurance requirement differently. Some insurance carriers will require a change of policy to meet the New Jersey increase, others will not provide insurance if you or any of your trucks travel into or through New Jersey and others require no change at all. Read more...

Not all Cargo Insurance is Created Equal

From time to time I, Joel Baker truck driver, have been asked by a customer or a broker if my insurance is from xyz insurance company. When I respond and say: “no, why do you ask?” I typically get a reply that goes something like “our company doesn’t, can’t or isn’t able to do business with any trucking company who has their insurance from xyz insurance company.” Usually what they are politely trying to tell me is that the customer or broker has had a previous bad experience with xyz insurance company in the form of a denied claim. Read more...

BEFORE Signing a Lease Agreement for a Truck – Check the Insurance Requirements Within the Lease Agreement.

There are pros and cons for both purchasing and leasing trucks as I wrote about several years ago in my Buying vs Leasing article. However, for those who wish to utilize the leasing option, there is a commonly used condition within lease agreements that can be a serious obstacle to overcome. Read more...

The Most Under-Appreciated Insurance Coverage in all of Trucking

If we don’t have this coverage, or if we choose to purchase only the minimum of this coverage, we won’t realize the mistake until it’s way too late.

A recent customer claim has solidified my opinion to never overlook or trivialize any of our insurance coverages. Read more...

Broker Agreements and Contracts

Brokers and customers frequently require to be added to our policy as an additional insured. This is a covert means to gain free insurance from us as well as avoiding financial responsibility when or if they cause us bodily injury or property damage.

A lesser known, but even worse, condition often included in a broker’s or customer’s agreement or contract is something called a waiver of subrogation.

Read more...

Leasing out Equipment?

If you have trucks and/or trailers sitting in the parking lot and you’d like them to generate some revenue to help pay the bills by leasing them to a third party company or an independent owner-operator, you’d be wise to contact your insurance agent first. Read more...

What goes into calculating your trucking insurance premium rate?

In 1999 I decided to apply for my own authority. But before doing so I wanted to make sure I had all my ducks in a row. I began to prepare. Secured the money for the down payment on a truck and trailer, saved enough operating capital for a minimum of 30 days, established a customer base, and developed a financial back-up plan if things went south on me. With all those items in place I was confident I had planned well and was prepared to get my own authority. I promptly did so. It wasn’t until I became an insurance agent that I discovered my plans should have started years earlier. Read more...

Additional Insured

Adding an “Additional Insured” is an endorsement. An “Additional Insured” endorsement does exactly what it sounds like it would do. It adds another party, in this case a customer or truck broker, to the policy as an insured. When an “Additional Insured” endorsement is added, there is a change made to the policy. It specifically extends insurance coverage to the “Additional Insured” customer or truck broker placed on the policy. Read more...

Why Every Truck Owner Should Read Their Insurance Policies

You might be very surprised to find what is NOT covered that you think you have coverage for & What is required of you to avoid a claim being denied or your insurance being canceled!

You’ve probably noticed an underlying theme in the majority of my articles here on Overdrive: The need to understand our insurance policy. All too often, we simply assume we know what we have for insurance or believe our insurance agent has told us everything we need to know about our policy. That includes me before I became an insurance agent. Assuming, though, is always a bad idea, especially when it comes to insurance. Read more...